Key Takeaways

- Annuity tables are user-friendly tools that simplify calculating an annuity’s present value.

- Annuity tables are not as precise as calculations made using annuity calculators and spreadsheets.

- Though not as precise, annuity tables are simpler to understand and easier to use than other methods of calculating the present value of an annuity.

There are many reasons you might want to know the present value of your annuity. Chief among them is the ability to tailor your financial plan to your current financial status. The present value of your annuity is a component of your net worth, and you need this information to ensure a comprehensive picture of your finances.

What Is an Annuity Table?

An annuity table, or present value table, is simply a tool to help you calculate the present value of your annuity. As Alec Kellzi, CPA at IRS Extension Online, told us, “These tables provide factors that are applied directly to the annuity payment amount and eliminate the need for complex calculations.”

Essentially, an annuity table does the first part of the math problem for you. All you have to do is multiply your annuity payment’s value by the factor the table provides to get an idea of what your annuity is currently worth.

Annuity tables also provide a standard that can fairly value annuities of different amounts. The IRS uses standardized annuity tables to value certain types of annuities for tax purposes.

The present value of an annuity is the current value of all future payments you will receive from the annuity. This comparison of money now and money later underscores a core tenet of finance – the time value of money. Essentially, in normal interest rate environments, a dollar today is worth more than a dollar tomorrow because it has the ability to earn interest and grow with time.

Thomas J. Brock, CFA®, CPAInvestment, Corporate Finance and Accounting ExpertThomas Brock, CFA®, CPA, is a financial professional with over 20 years of experience in investments, corporate finance and accounting. He currently oversees the investment operation for a $4 billion super-regional insurance carrier.

How To Use an Annuity Table

To use an annuity table effectively, you first need to determine the timing of your payments. Are they received at the end of the contract period, as is typical with an ordinary annuity, or at the beginning? Because most fixed annuity contracts distribute payments at the end of the period, we’ve used ordinary annuity present value calculations for our examples.

- 1. Identify the interest rate and the number of periods.

- You’ll need to know your number of payments and interest rate, which can be found in your contract.

- 2. Find the PVIFA on the table.

- An annuity table gives you the present value interest factor of an annuity, or PVIFA. The annuity table is usually structured with interest rates on one axis and the number of remaining payments on the other axis. You find the PVIFA by locating the intersection of your interest rate and the number of remaining payments on the table.

- 3. Calculate the present value.

- Once you have the PVIFA, you simply multiply it by the amount of each payment in your annuity. The result is the present value of your annuity.

Here’s a step-by-step explanation of how to use an annuity table to bypass the most complex step in traditional present value calculations:

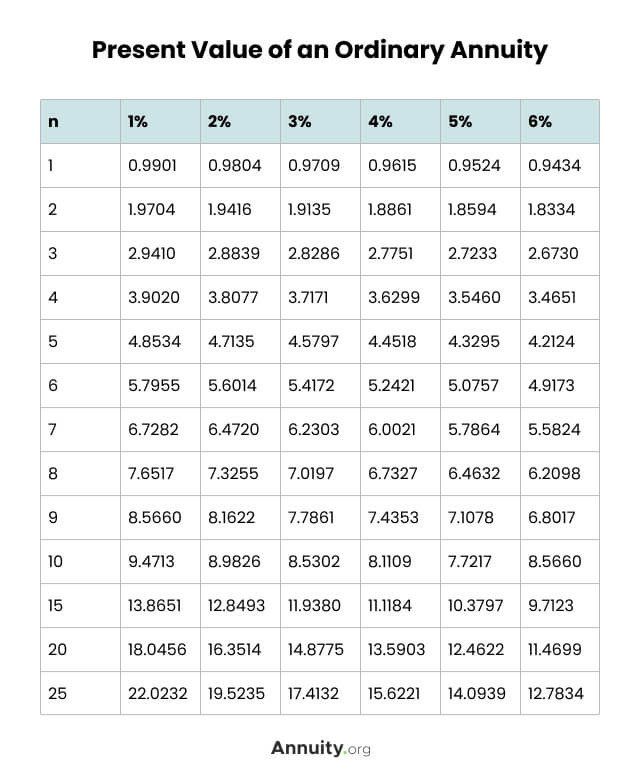

Below is an example of an annuity table for an ordinary annuity. Remember that all annuity tables contain the same PVIFA for a specific number of periods at a given rate, much like multiplication tables give the same product for any two numbers. Any variations you find among present value tables for ordinary annuities are due to rounding.

Annuity Table for Ordinary Annuities

| n | 1% | 2% | 3% | 4% | 5% | 6% |

| 1 | 0.9901 | 0.9804 | 0.9709 | 0.9615 | 0.9524 | 0.9434 |

| 2 | 1.9704 | 1.9416 | 1.9135 | 1.8861 | 1.8594 | 1.8334 |

| 3 | 2.9410 | 2.8839 | 2.8286 | 2.7751 | 2.7233 | 2.6730 |

| 4 | 3.9020 | 3.8077 | 3.7171 | 3.6299 | 3.5460 | 3.4651 |

| 5 | 4.8534 | 4.7135 | 4.5797 | 4.4518 | 4.3295 | 4.2124 |

| 6 | 5.7955 | 5.6014 | 5.4172 | 5.2421 | 5.0757 | 4.9173 |

| 7 | 6.7282 | 6.4720 | 6.2303 | 6.0021 | 5.7864 | 5.5824 |

| 8 | 7.6517 | 7.3255 | 7.0197 | 6.7327 | 6.4632 | 6.2098 |

| 9 | 8.5660 | 8.1622 | 7.7861 | 7.4353 | 7.1078 | 6.8017 |

| 10 | 9.4713 | 8.9826 | 8.5302 | 8.1109 | 7.7217 | 7.3601 |

| 15 | 13.8651 | 12.8493 | 11.9380 | 11.1184 | 10.3797 | 9.7123 |

| 20 | 18.0456 | 16.3514 | 14.8775 | 13.5903 | 12.4622 | 11.4699 |

| 25 | 22.0232 | 19.5235 | 17.4132 | 15.6221 | 14.0939 | 12.7834 |

Annuity Tables and the Time Value of Money

Annuity tables estimate the present value of an ordinary fixed annuity based on the time value of money. Consider that every dollar has earning potential because you can invest it with the expectation of a return. The time value of money principle states that a dollar today is worth more than it will be at any point in the future.

Imagine you have $1,000 right now and you deposit it into a high-yield savings account offering a 1% annual interest rate. By the end of the year, your balance would grow to $1,010 because of the interest earned.

If you were to receive $1,000 at the end of the year instead, you would only have that $1,000. In this scenario, the future $1,000 is effectively worth $990 today because you missed out on the opportunity to earn that 1% interest over the year.

While this example is straightforward because it involves round numbers and a single payment period, the calculations can become more complex when dealing with multiple payments over time.

That’s where an annuity table comes in handy. The table simplifies this calculation by telling you the present value interest factor, accounting for how your interest rate compounds your initial payment over a number of payment periods.

Get Your Free Guide to Annuities

How To Use the Present Value of an Annuity Formula

While an annuity table provides a quick and easy way to calculate the present value of an annuity, it’s not the only method. Another approach is to use the present value formula. This mathematical equation, while more complex, is more precise.

The formula for finding the present value of an ordinary annuity is often presented one of two ways, where “r” represents the interest rate and “n” represents the number of periods. Using either of the two formulas below will provide you with the same result.

In the PVOA formula, the present value interest factor of an annuity is the part of the equation written as multiplied by the payment amount. If you consult an annuity table, you can easily find the PVIFA by identifying the intersection of the number of payments (n) on the vertical axis and the interest rate (r) on the horizontal axis.

Other Methods for Calculating the Present Value of an Annuity

There are still other methods for calculating the present value of an annuity. Each has a different level of effort and required mathematical skills.

Using an annuity calculator or a financial spreadsheet set up for calculating the present value of an annuity is often more precise than using the preset annuity table. These tools are also helpful if your values fall outside the annuity table’s given ranges.

Say you own a fixed annuity that pays a set amount of $10,000 every year. The terms of your contract state that you will hold the annuity for seven years at a guaranteed effective interest rate of 3.25%. You’ve owned the annuity for five years and now have two annual payments left.

You could find the exact present value of your remaining payments by using a spreadsheet, as shown below.

Frequently Asked Questions About Annuity Tables

Annuity tables are visual tools that help make otherwise complex mathematical formulas much easier to calculate. They lay the calculations for predetermined numbers of periodic payments against various annuity rates in a table format. You cross reference the rows and columns to find your annuity’s present value.

A present value annuity table provides a simplified method to calculate the present value of an annuity, which is the total value of a series of future payments at a specific interest rate, by providing the present value interest factor of an annuity (PVIFA).

Calculating the present value of an annuity can help you determine whether taking a lump sum or opting for future annuity payments spread out over many years will be more beneficial to your financial needs or goals.